Key Takeaways

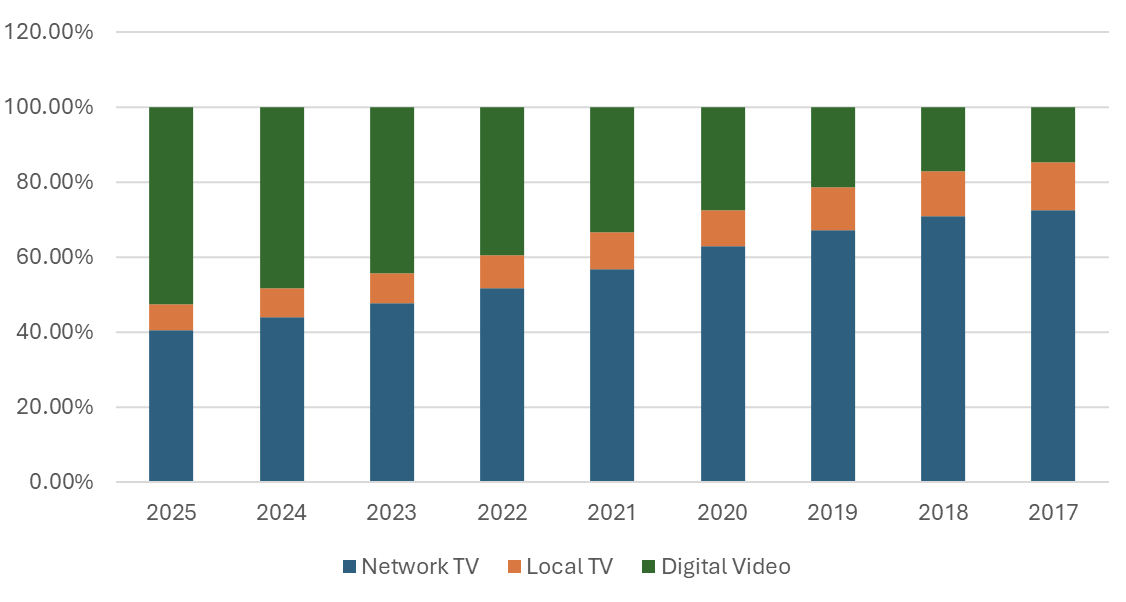

- Local TV’s share of total media spend has declined from 13% in 2017 to just 6% by mid-2025, as digital video buying becomes more accessible across advertisers of all sizes

- Automotive, Entertainment & Media, Financial Services, and Technology account for nearly 70% of Local TV investment, yet all four categories posted double-digit YoY declines in 1H 2025

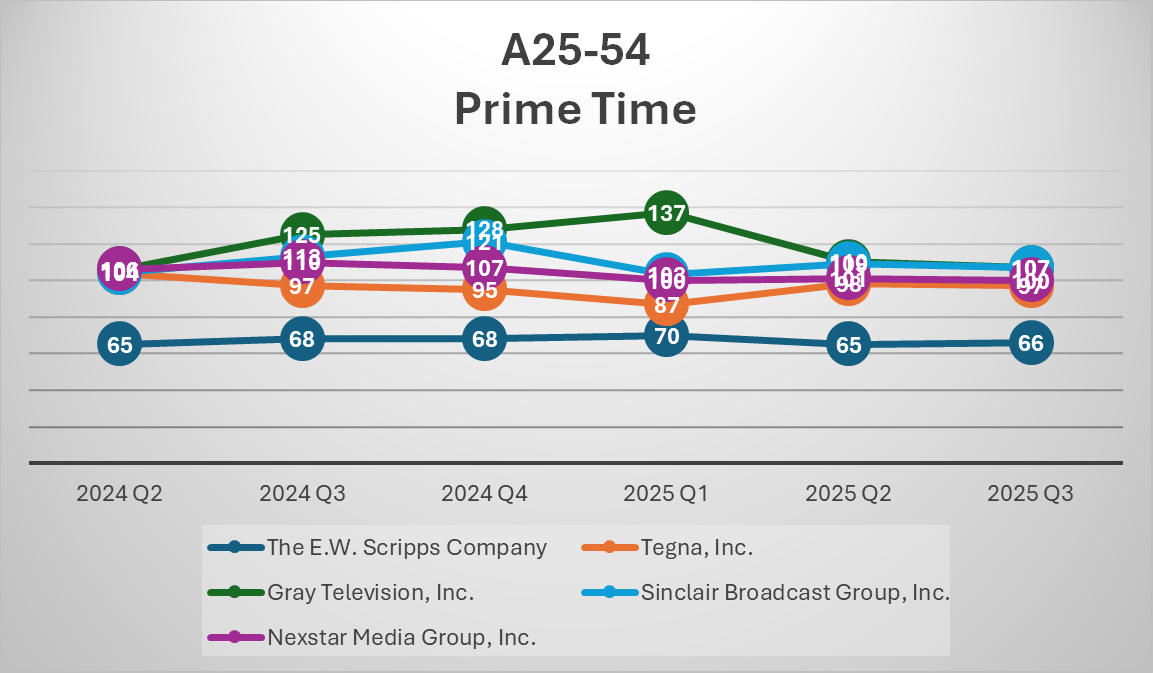

- CPM indices reveal widening pricing disparities across station groups — with Gray Television and Sinclair trending above market medians, while Tegna and Scripps discount below 100, indicating that consolidation among major station groups could reshape pricing power and bargaining dynamics

A Shifting Media Landscape

Local TV is navigating one of its most significant resets in decades.

Guideline data shows that volatility in Local TV spend long predates the disruptions of COVID-19 — reflecting deeper, structural challenges tied to consolidation, platform competition, and advertiser reallocation.

As Digital Video’s share has doubled since 2017, Local TV’s has halved.

At the same time, mergers among major station groups (like Nexstar Media Group) are consolidating scale and negotiating leverage, altering the economic balance between local broadcasters and national buyers.

Pricing Power and Market Consolidation

As spend fragments, pricing power tells a different story.

Guideline’s Weighted CPM Index measures how Local TV station groups price relative to their market norms. Each group’s CPMs are normalized to a median of 100 for their local market, then weighted by market size — meaning larger DMAs carry greater influence. The result reveals which owners command consistent premiums (strong pricing power) versus those who discount below market medians. The results reveal a meaningful divergence among the five largest Local TV owners:

- Gray Television and Sinclair Broadcast Group consistently trade above market medians, signaling strong pricing control

- Tegna and Scripps remain below 100, discounting relative to peers

- Nexstar continues to command premium CPMs across Prime Time and Late News

Together, these trends highlight how Local TV’s value equation is evolving from with pricing driven increasingly by ownership strategy and audience composition rather than broad demand.

Looking Ahead

Local TV is not disappearing — it’s redefining its role.

As digital platforms absorb lower-funnel activity, Local TV is repositioning around credibility, reach, and regional relevance.

Its long-term success will depend on how effectively broadcasters integrate with digital video ecosystems and prove measurable, cross-channel impact.